The divergences principles, which states that price action must be accompanied by the internals of the market. Back in early March, price in the form of lower lows wasn't being matched by the internals, which are measured by momentum and MACD.

Well, guess what? That exact same set of circumstances is now in play,

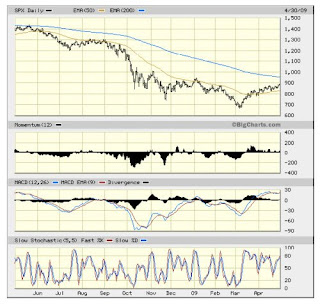

only in reverse - higher highs aren't being matched with strength in momentum and MACD (first and second indicators below price). This can be seen very clearly in the accompanying S&P chart above.

Moreover, as was the case back in early March, these conditions are nearly across the board, as the divergences aren't exclusive to the US major indices. Even the strongest of the strong in this rally -- such as emerging market, Brazil -- has nearly exactly the same set of divergence conditions setting up (higher highs in price, non-confirmation by both momentum and MACD).

As if that wasn’t enough to cause a bullish investor some concern, the very short-term indicator I track, Slow Stochastics, is edging toward an overbought reading (>80), which tilts the odds even more in favor of a market stall if not outright decline.

In my experience, when both sets of indicators -- one measuring the near-term strength, the other the very short term -- are flashing warning signs, it's advisable to be more than a touch more cautious, especially after stocks have rallied 32% off its devilishly low of 666 (

S&P 500).

The last area to explore is the historical record. Sam Stovall, Chief Investment Strategist with S&P, produces some of the very best historical data around. In one of his most recent commentaries, he notes:

“Since 1929, the S&P 500 gained 4.8% from November 1 - April 30 versus 1.6% from May 1 - Oct. 31. Also, the November - April period beat the May - October period 68% of the time. Yet after bear market bottoms, the S&P 500 gained an average 12.2% in May - October and advanced in 12 of 14 observations.”The key phrase in Sam’s comments is “after bear market bottoms,” which means you have to buy the idea that the November 2008 lows was

the low. In this regard, I'm not in that camp just yet. That’s not to say I think we'll take out the November low, but that things are much too fluid -- the stress-test results to be released next Monday being the most immediate area for concern -- for me to base my investment-strategy decisions on a high-risk "maybe."

Many of you are familiar with Gann’s Panic Zone for bottoms of 49 days (7 squared to 55 days)--the same timing can often times be used to find blowoff tops: Friday 24th April, was the 49th day from the March 6 low.

The Wheel of Time and Price suggest that another break of 856/860 support level should magnetize the S&P down toward 800.

Why? 860 is opposition the March 6 low - a second break of this level suggests lower prices. It implies that the S&P has been churning around this level and that the action has been distributive. At the same time, 803 is on the same "vector" - opposition 860 and conjunct March 6 (i.e., 180 degrees down in price).

790 is a corrective 270 degrees down in price from the 875 high.